Here's another idea which may or may not works.

Liberty Media is due to spin off its non-Starz related assets, i.e., its media investment assets in Sirius XM, Live Nation, Barnes & Noble, minority interest in Time Warner, Viacom, Sprint, etc.

According to this press release (http://ir.libertymedia.com/releasedetail.cfm?ReleaseID=732276), persons acquiring Liberty Media common stock in the market through Jan 11, 2013 will receive shares of Spinco common stock in the distribution. So people who buys LMCA at $122 today will still qualify for shares in the Spinco.

And the Spinco stock is now traded on as "when-issued" basis on Nasdaq under the stock code, LMCAV (http://www.nasdaq.com/symbol/lmcav). "When-issued" refers to the stock price as if the stock is selling on the day it is ex-dividend or ex-distribution or rights. It closed at $108.71 yesterday.

So if you buy LMCA at $122, and on Jan 14, 2013 (coming Monday) when it is ex-distribution and if the actual price then really tracks the "when-issued" price of $108.71, you are actually paying $13.29 per share of Starz stock.

Upon completion of spin-off, there'll be about 124 million outstanding common stock in Starz. Starz makes $240 million in 2011. Thus, eps is $1.93. At the price $13.29, it priced at 6.88x earnings - a value too low compared to other cable companies like AMC Network (>17x) or Discovery Communications (>20x). Even if we use a conservative valuation at 12x eps, it is worth at least $25.

So by paying $122 today for LMCA, you get 1 share of Starz on coming Monday. If you can then sell the non-starz stock on Monday at the same price as the "when-issued" price traded last night at $108.71, you are only paying $13.71 for each Starz shares which produces earnings of $1.94 per share.

Easily, you can almost double up your capital of $13.71 to $25 based on 12x earnings of Starz.

Disclosure: I bought some LMCA at $120.7.

Friday, January 11, 2013

Friday, January 04, 2013

Review of Portfolio for Y2012

Let's

start with recent comments from Seth Klarman:

'The

key watchword for the first half of the year [2012] was patience. We

patiently sifted through scores of interesting investment ideas to

find only a few really good ones. We patiently held cash while

waiting for prices to hit our buy levels before accumulating. We

stayed abreast of the U.S. markets where most of our investments

reside, while patiently searching European markets for the occasional

morsel, despite the frustrating reality that most sellers continue to

cling tightly to their troubled assets--at least for now. All the

while, we built up our knowledge of European markets, country by

country and asset class by asset class, while expanding our base of

relationships and developing price targets for many businesses and

assets that we would love to own at the right valuation, awaiting a

reckoning that we deem likely to come but at a date uncertain.' -

Seth Klarman

We

agree patience is key particularly in times when few investments are

available to deliver an above-average historical return. But a lack

of good investment opportunity does not mean the next move is

downwards for the market. With huge liquidity flooding the system, we

can understand why the market is going up. Fed, for one, is pumping

$85b a month ($45b on long term treasury and $40b on mortgage backed

securities) into the system, although in the latest Fed's minutes, it

hinted that stimulus may be ended earlier than expected. That is over

a trillion dollar of monetary stimulus that is rushing into the

market annually. Couple with ultra-low interest rate which is

expected to be near zero until unemployment rate reaches 6.5% or

below, there is little places to stash one's cash for a decent but

risky return. For those who keep cash, it has less buying power as

time passes. Thanks to the Fed, savers find themselves subsidizing

enterprises and corporations. It is essentially a transfer of wealth

from savers to corporations. Just that it is done stealthily. Not

only is it done stealthily, but it also punishes the responsible

savers while rewarding and subsidizing those who took excessive risk,

bought houses they could not afford or had otherwise ran up too much

personal debt. For savers who realize they are “conned,” they may

then opt to invest in other asset classes like corporate or sovereign

bonds or even equities just so that they do not get “conned”

again. That's why we hear more people saying it is better to buy

dividend assets than to have cash. Eventually, these savers may find

themselves getting “conned” again by the macroeconomic policies

which had driven or “coerced” them to invest in such assets

classes so just that they are able to maintain their real net-worth,

which they otherwise would not have had interest rate been more

normal, when things come to a head. This is exactly the time when

things get more risky when everyone is heading in the same direction.

In short, investors are hugely influenced by what Fed does. Today,

Fed is telling us to go forth and speculate and I don't care what you

buy as long as you buy.

Given

the current situation, we think it is hard to short the market given

that the liquidity have to go somewhere, at least for the short term.

With stimulus, not only monetarily but also fiscally, couple with low

interest rate, many are enticed or “forced” to get invested so as

not to see their “real” net worth gets decimated by the negative

real interest rate. Negative real interest rate is likely to persist

for some time and thus, we can understand why people are putting more

of their savings in assets that provides better yield than normal

savings interest-bearing account.

Although

we doubt the market will suffer a big crash any time soon, that does

not mean it would not. We are mindful that the possibility of a

correction is always there. Washington has simply deferred the fiscal

and debt ceiling issues. End of February, Congress must boost the

federal borrowing limit. On March 1st, $110 billion of sequestration

or automatic spending cuts begin slicing into defense and domestic

spending if no deal is reached. By end of March, a government

shutdown looms unless Congress approves funding for government

operations for the reminding of the fiscal year, which ends Sept 30.

Without action, many federal employees could face the possibility of

being furloughed. Although Washington is dysfunctional and has

provided band-aid fixes so far, we believe Winston Churcill is right

when he said: “Americans

can always be counted on to do

the right thing after

they have exhausted all other possibilities.”

But we do not know if they are at the end of the road yet or still

has more possibilities to exhaust and drag for more time.

So

all these are affecting business decisions who typically plan on a 3

or 5 year basis. How do we expect businesses to plan if they do not

know what is going to happen in a few months? But regardless,

liquidity is flooding the market and there is some tailwind behind

the U.S. economy driven by the housing and automotive sectors. Annual

U.S. automotive sales may potentially even rise to pre-recession

highs.

But

what is likely to happen two or three years from now when

unemployment hits 6.5% or even 6%, when monetary support is

withdrawn, would the economy be able to stand up on its own, how

about inflation, and how about when interest rate goes up? We do not

know the answers and do not attempt to be part of the jury. We just

play to our strengths which is to look on a bottom-up basis. For us,

we think capital preservation is more important than to rush into

deploying capital so just as to maintain our real net-worth. We fear

the alternative may be worse when things come to a head. Because in

times of chaos, cash is probably the only asset that is certain to

hold up the best in terms of value which you can then use as the

currency of choice to purchase what others deem as trash and risky,

and thus rush to sell regardless of the underlying value.

An

investor who invests just based on the relationship between interest

rate and inflation in order to maintain their real worth is missing

another ingredient to the equation: risk. Example, for bonds, prices

are high but yield is low though it meets savers' goal of exceeding

banks' savings interest rate but the proposition is risky with

current bond prices. Part of the risk facing investors is that the

math on bond prices and yields means it won't take much higher yields

to inflict substantial capital losses. With 10-year Treasury yielding

1.7%, a one-point rise in yield would lead to a 9.2% decline in the

value of bonds. For investment-grade corporate-bond index of 5 to 10

year notes, a one-point increase in yields would cause a 6.4% drop in

bond value. So in chasing to maintain real “net-worth” may or

will ultimately cause one to worth less.

So

investors find themselves between a rock and a hard place, facing

either the likely but limited erosion of purchasing power that

originates from holding cash, or the uncertain but potentially

disastrous impairment of capital that arises from owning overvalued

equities or bonds. Both are unappealing choices but we prefer the

former.

And

what makes this choice harder is how long will the negative real

interest rate last, this will make a difference to an investor's

choice in equity or cash. There's no easy answers to the problem of

real capital preservation in an age of financial regression, only

difficult choices.

Depending

on how long the financial regression lasts, if we assume it is

short-lived, then it may be wise to be underweight equities and

conserve capital and wait a riper opportunity set by out-compounding

the drag of inflation and negative real interest rates.

We

do not know when market will bust and neither do we intend to time

the market. We just simply play to our strength and evaluate equity

by equity and if the price is good, we will buy it, regardless of

economic condition. That is why we build up our cash position in the

second half of 2011, peaking at 43% at end of 2011. But our cash

position has since dropped to 27%. Now you may question why did it

drop so drastically when we think there is both a lack of good

investment ideas and our intent to patiently hold cash until we find

a good investment. Here's the caveat: a lack of good ideas doesn't

mean there isn't any, we were fortunate to identify one area of

interest. So, substantially all of the drawdown of cash were spent on

two positions – Mastercard and Visa. Had we not spent on them, our

cash position would have increased. Thus, if we exclude Mastercard

and Visa, cash would have increased by 15 percentage points.

Portfolio

Performance (all results are based in terms of USD)

Figure

1.

{kind=link}

We

added a new table (figure 2) to show the performance purely on our

equities:

Figure

2.

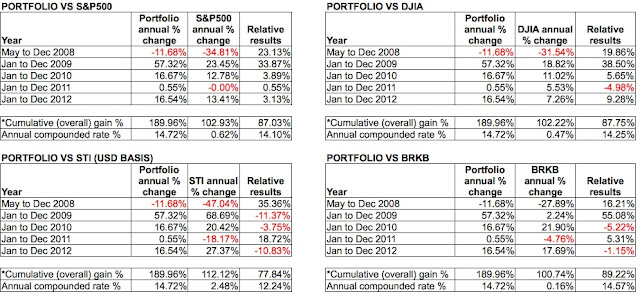

Our

portfolio return 16.5% for the year versus S&P500 13.4% (as can

be seen in figure 1). This is the 5th consecutive year we

are ahead of the most broad-based USA indices. We hope it is not

fluke and we endeavor to keep our eyes on the ball and the field, not

the scoreboard per se.

We

changed the starting date to measure our performance in year 2008

from 1st January to 1st May because it is the

actual inception month of our portfolio. Had we maintained January

for comparison, our portfolio would outperform S&P500 by 26.8% in

Y2008, compared to 23.1% from May 08 to Dec 08.

Although

we perform well this year even with substantial cash position, we

underperform the Singapore Straits Times Index by almost 11%. Most of the underperformance can be attributed to the fact that we are

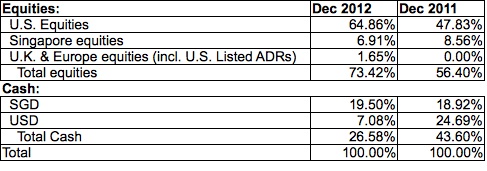

overweight on U.S. dollar assets. Figure 3 shows our distribution of

assets:

Figure

3.

We

are not concern about outperforming the benchmarks year after year,

although we understand it can be irritating not to. Instead, we aim

to outperform the major USA and Singapore broad-based indices over a

full economic cycle. Even though, we may lag the STI index by a huge

margin in 2012, we have however outperformed the index by an

aggregate of almost 78%, even with 3 years of underperformance out of

the 5 years since our inception in May 2008. We tend to outperform on

the downside than on the upswing. Our portion of Singapore equities

returned 23.1% against STI 27.4% (as can be seen in figure 2).

Capital

preservation is the most important thing to us. We will grow it with

the appropriate risk-adjusted return by managing risk rather than

swinging for the fences to maximize profit at all cost. We do not

have the gut to stomach significant losses. At times, we will make

mistakes, we are sure of that, but we will try to keep it at bay.

What

drove our returns?

Figure

4.

{kind=link}

From

figure 4, we can see the top 3 drove 66.8% of our equity gains in

2012:

- MasterCard and Visa – As a group, up 34.4% and makes up 43% of the total equities gain for the year. Individually, MasterCard is up 32.1% while Visa is up 47.3% and comprises 34.3% and 8.7% of our total equities gain for 2012.

- Berkshire Hathaway – Up 17.7% and comprises 19.3% of total gain.

- UOB – Up 31.4% and makes up 13.1% of total gain.

We started the

year with Berkshire Hathaway, PepsiCo, and UOB as the top 3 equity

positions – which makes up 69% of all equities held at the start of

the year. We did not own any Mastercard or Visa then. So 2 out of the

top 3 starting positions are the major drivers for this year

performance.

Mastercard and

Visa, which we bet aggressively by using almost 44% of our starting

cash ended comprising about 20% of our total portfolio, at the peak

(15% at end of 2012).

As for PepsiCo, we

sold all of it by May, at a modest gain from our cost.

Portfolio

Discussion

Figure

5.

We

ended 2012 with 21 equities, compared to 10 positions in 2011. Our

top 3 positions makes up almost 40% of total portfolio; top 5, 49%.

Excluding cash, top 3 makes up 54% of all equities, and top 5, 67% of

all equities.

Discussion

on equities

- Berkshire Hathaway: Our largest equity position comprises almost 17% of total portfolio. Berkshire is our longest holding stock. Although we adjust the position size from time to time, depending on value or alternative, we have maintained our current position size since May 2011.We bought our first share in Oct 2008 at a cost of $57. We think there's not much downside to the current price. BRK is prepared to repurchase shares at 1.2x of reported book value which is about $89 – $90 based on 3Q numbers. In fact we think the stated book value is substantially below intrinsic value. For example, Burlington Northern Santa Fe was purchased in 2010 for $34 billion. BNSF is expected to earn $3.5 billion in 2012. Using a multiple of 15x earnings (same as Union Pacific), BNSF is worth $54 billion. If accounting rules allow writing up of goodwill, then BRK book value will increase by $20 billion. Based on BNSF alone, the stated book value as of 30 Sep 2012 is at least 10% less if we include the $20 billion increase in BNSF's value.For more details on BRK valuation, we think Whitney Tilson provides a good presentation on it. You can google for it. In the past, we have made some money from Tilson's idea – Anheuser-Busch InBev, although we sold it early. He was spot-on on that, in fact, BUD went even further than what he thought will sell for – currently BUD is selling for $87 versus his target of $72 or so.

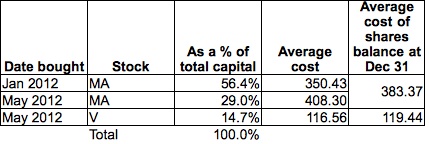

- Mastercard and Visa:

Figure 6

We bought

Mastercard and Visa in two batches – January and May 2012. We

allocated 56.4% of the total capital during January 2012, all on

Mastercard at an average cost of $350.43. Subsequently, we added

more and allocated the rest of the capital related to them during

May 2012: at an average cost of $408.3 for Mastercard and $116.56

for Visa. Our average cost for the two batches of Mastercard is

$368.15. Subsequently, we reduce some of the holdings, Mastercard

was reduced by 33.9% and Visa by 12.8%. As a result, our average

cost for the rest of the shares remaining at year end is $383.37

for Mastercard and $119.44 for Visa. In addition to selling our

holdings, we did some rebalancing between the two counters during

year: for example, when Visa is cheaper than Mastercard, we sell

some Mastercard to hold more Visa, so it resulted in a higher

reported average cost per share in Visa at $119.44 than the

original cost of $116.56 but overall, it benefited our holdings

than if we had not rebalanced.

At year end, both the stocks

comprise about 15% of total portfolio with Mastercard making up

about 12.4% and Visa 2.7%. Both have about the same potential

medium term growth – 15 to 17%. But Mastercard is priced slightly

cheaper than Visa. At current price, we think both are fairly value

at 19 to 20x forward earnings. We won't be expecting any outsize

return from them. But they should still bring us reasonable return

simply by rising at the same rate as earnings without relying on

any expansion in earning multiples. Even if the price remains the

same a year from now, we think it provides a good entry point to

add more given that the then valuation is likely to be less than

17x on a forward basis. If either one of them falls, say by 10%, in

a year time, we will shift more of our assets into them because

valuation would likely be close to 15x forward earnings.

We think

the long term prospect is very bright – payment is in a secular

growth market. More transactions in the future will be done

cashless, especially for market outside of the U.S. where

transactions are still largely done in cash. In U.S., 29% of all

retail transactions are in cash, down from 36% a decade ago.

According to Mastercard, 85% of all global transactions are in

cash. The huge gulf in cash transactions between the U.S. and

globally lies in the emerging markets. Cash still largely prevails

in emerging markets because of the slow development in electricity

and communication infrastructures. However, smartphones and

wireless networks should help to bridge these physical

restrictions.

There are a lot of competition in the payment sector

from PayPal operated by Ebay, Google Wallet, Square, among others.

But all of them operates in the digital wallet space, essentially a

locker of personal-payment data stored either in the cloud or on

smartphones. None of them have made a dent to the network

infrastructure that facilitates the actual flow and transfer of

money between merchants and financial institutions in the credit

and debit space. PayPal acts as an acquirer which is the

institution that acts on behalf of a merchant to process debit and

credit payments. And acquirers need the network infrastructure such

as Visa to facilitate flow of payments between the merchant bank

(acquirer) and the customer banking facility (the card issuer) –

just like if you and me want to talk on the phone, we need the

phone operator and Mastercard and Visa is the phone operator in the

payment space. Mastercard and Visa also have their own operations

in digital wallet, called PayPass and V.me. But when it comes to

routing transactions, essentially the infrastructure that connects

and sits between the merchants and banks, Mastercard and Visa are

the dominant players.

Digital wallet, despite all the hype, has

thus far done little to alter the relationship that has been built

around credit and debit. Compared to Amex and Discovery Financial,

Mastercard and Visa have lesser business risk, though it may be

riskier for an investor in terms of the higher stock valuation –

Mastercard and Visa sells for high teens to low twenties multiple

while Discovery and Amex sells for high single digit and low teens,

respectively. Amex and Discovery, like Amex, in addition to

providing a payment network also provides financing to their

customers, so they have more risk associated with credit. Whereas

for Mastercard and Visa, they are pure-play payment network. Their

revenue comes from fixed per-transaction fees, service fees based

on transaction size, and fees for cross-border transactions. Visa

and Mastercard make about 10 cent for every $100 transaction.

So even if there is inflation, we think Mastercard and Visa

provides very good hedge.

Adding to Mastercard and Visa moat is the

trust that exists between the banking institutions and them, which

essentially allows them to reach into customers' banking accounts

and subtract money. And banks like the status quo especially when

the banks take most of the fees that flow through the card

networks. In effect, the banks play a big part in protecting the

domain of Mastercard and Visa. Moreover, their business model held

up extremely well during the 2009 crisis, revenue for both rose -

Visa by 9% and Mastercard by 2% - with operating earnings rising at

a much higher pace. It was the first time their business model is

tested as a public company and they passed with flying colors.

Although the shares were sold off at that time, investors now know

how resilient their business model is. So even if there's a

recession, we think Mastercard and Visa is likely to hold up much

better than the last time and better than most other businesses.

Even in a recession, we think they should be able to deliver growth

in earnings per share because they have a number of levers to pull.

For example, both of them are essentially free of debt, so if they

want to orchestrate a huge repurchase of shares, it is one lever to

use. In fact, we will be happy the shares plunge so that we can buy

more while the companies are also buying back an undervalued share.

Another lever is they can easily cut back on expenses especially

marketing related – the kind of expenses that can easily be cut

in a downturn – that is what Amex did during 2009, so if Amex

can, we are sure Mastercard and Visa are able to as well.

- DirecTV: 57.4% of the positions are purchased at an average of $44.22 from Dec 2011 to May 2012, and the rest were acquired in October 2012 at an average of $51.43. We recycle part of the proceeds from Mastercard and Visa in DTV during October. At $51, stock is priced at 10x 2013 earnings. We think it trades at a significant discount to intrinsic value and offers steady, leveragable cash flow, exposure to Latin American growth and sound capital discipline. DTV started the year as our smallest equity position with less than 2% of total portfolio. But it ended as our 3rd largest equity position with slightly over 10% of total portfolio.We think DTV is one of the cheapest play within the pay-tv sector, whether we use the traditional PE or EV/EBITDA valuation. Dish Network, a pure satellite pay-tv play, is the closest comparable that sells for 15x earnings, almost 50% more than DTV valuation. For others, like Time Warner Cable, sells for 14x earnings. However TWC is more than pay-tv, it provides internet and phone services as well, which provides an advantage over pure CATV play since TWC can provide so-called “triple-play” package to entice new sign-ons and also provide a leverage to reduce churn rate. But is “triple-play” advantage worth to pay 40% premium more? We are cheap so we will play it cheap and hopefully, the difference in valuation will close up in DTV's favor.

- IBM: Makes up 7.1% of total portfolio. All of the positions were initiated in 2012 between $180 to $198, at an average cost of $193.18. We think IBM has a good chance of performing well in 2013 partly because of the easy comps which reset the forward benchmark to a lower hurdle to cross, in terms of the Street expectations. We also like that about 60% of IBM profit is recurring nature due to its large software (23% of revenue) and services (58% of revenue) that have longer-term multiyear contracts. As a result, its business performance have been less volatile and more predictable than most.But one of the things we did not like is the way it reported earnings in Q3 when its reported adjusted operating earnings include a one-off gain from the sale of a line of business to Hitachi. If it is a one-time gain, why is it part of adjusted operating normal profit? We cannot understand except to the extent that the corporation try to mask the underlying performance and hope that others miss it. And none of the major news media spotted it, or at least reported it. Nonetheless, we still think IBM should perform decently for the next few years and has a reasonable chance to achieve its stated roadmap of $20 of operating earnings in 2015. But we will keep a close look on them quarter to quarter on the reporting and underlying fundamentals.

- Stocks that makes up 2 to 3% of portfolio: We hold 5 stocks which each makes up between 2 to 3% of total portfolio each. In total, these group makes up 12.1% of total portfolio. The 5 stocks are Visa, UOB, Dollar Tree, Johnson & Johnson, and IAC/Interactive.

- UOB – We bought it during Q3 of 2011. We have reduce 2/3 of our UOB holdings this year. We don't think it is expensive, especially compared to most other STI components. It has roughly played out as what we think it should have. The bank has grown its asset base as we think it can. If return on asset returns to 1.2 to 1.3%, it can earn between $1.75 to $1.9 based on $230 billion of assets, valuing the current price at 10-11x earnings.

- Dollar Tree: We acquired during Oct 2012. Up less than a percent. Stock is down quite significantly from the high. In fact, all the Dollar stores are way off from the high, and valuation are roughly the same among all the three – Dollar Tree, Dollar General and Family Dollar – valued at about 14x forward 12 months earnings. For us, we are more attracted to Dollar Tree because it is the least leveraged and has the lever to pull on that basis if needed or maybe it will appeal to certain private shop given the low leverage and strong cash flow.

- IAC/Interactive: Acquired in Q4 at an average $48.27. Down 2% so far. Usually we do not invest in technology but we think IAC provides good value for the type of growth it guides for. Sells for 13x earnings, and 11x ex-cash for 2013 earnings. We also like that Barry Diller is the head of the company. We think of Barry Diller in the same breath as John Malone – both of whom have proven to unlock value and deploy capital efficiently.

- Johnson & Johnson: JNJ is the second longest holding in our current portfolio. We have held them since 2010. Up 6.9% in 2012 and up 14.6% from acquisition.

- We own another 12 equities which in total makes up 14.9% of total portfolio. Following are the equities:

- Tesco: Acquired in January 2012 at an average cost of US$4.94 – up 13.3%. If we did not elect to take one of our dividend in script, we will up 9.8% instead.

- CSX: Acquired in Q3 2011. Up 2.6% for the year and up 9.3% from cost. We reduced over 60% of the positions during February 2012. Results has been tepid mainly due to the depressed natural gas prices which drive lower demand for coal. Although coal makes up a huge chunk of CSX business (over 30%), strong growth in automotive and intermodal has largely offset the decline in coal volume.

- Celgene: Acquired in May 2012 at a cost of $71.34. Up 10.2%. We reduced 46% of the positions in October 2012. However, we think still Celgene should provide decent return. If EMA approves Revlimid as a first-line treatment for Multiple Myeloma, it should give some tailwind to the stock. Even if it doesn't, Revlimid is already prescribed off-label as a treatment for MM in Europe. Also, Celgene has some recent success in clinical trials for the cancer drug, Abraxane, resulting in approval for extended use in metastatic non-small cell lung cancer. There are other trials in the pipeline for Abraxane for other form of cancers, for example, pancreatic. We think there's a decent chance in will sell for $90, for 16x 2013 earnings.

- Norfolk Southern: We initiated NSC in the first two months of 2012 and ended comprising over 5% of our portfolio at that time. Subsequently, we reduced 70% of our holdings in the middle of 2012, at a modest loss of 1%. The cost for the remaining shares is $71.4, down -13.4%. Inclusive of the shares sold, we are down – 4.7%. Norfolk Southern has basically the same business model as CSX in which coal is pressurizing the underlying business. We think a lot of the bad news are priced into the current price. To go much lower, we think the economy needs to stop in its track.

- Coca Cola: We sold all of our Coca Cola shares in the middle of the year and then again initiated a small stake in Dec 2012 for $36.49. The earlier stakes were sold at a gain of 12%, which were acquired in Nov 2011 and Jan 2012 at an average price of $33.38. We think the current price is a reasonable entry point to pay for a business of Coke quality at 16.7x 2013 earnings. Together with the earlier stake, Coke returned 8.9% for the year, and 11.2% from cost basis.

- American Express: Bought in Oct 2012 at $56.75. Up slightly at 1.3%. Valuation is not particularly demanding at 13x 2012 and 12x 2013 earnings.

- National Oilwell Varco: We did not pay much attention to the oil and gas sector (especially contractors that serve the exploration of oil) until August this year when Berkshire Hathaway initiated a position in the stock. The stock then was selling for over $80 a share and peaked at $89.95 in Sep 2012. Then it fell to about $80 and generally sells between $77 to 83. It took a big correction in December 2012, falling to a low of $64.82. During the time from August to December, we spent some time familiarizing with the oil and gas sector, particularly on the upstream operations including on and off-shore drillings. Fortunately, our time spent paid off somewhat when NOV fell below $70, a price we think provides a good entry. We finally took a small bite and acquire some at $66.9. NOV is the dominant equipment provider for oil and gas drillers, both onshore and offshore. Its share grew by 5-folds in the past decade largely due to its success in persuading drillers in the early 2000s to shift from custom-built rigs to rigs built around its own standardized components, according to Morningstar analyst Stephen Ellis. Today, an overwhelming majority of rigs use NOV's parts. Vendors cheekily called them: “No other vendors.” NOV is largely dependent on energy prices which drives drilling activities. If oil prices doesn't support drilling activities, NOV business will be adversely affected. However, NOV is among the safest energy plays because it serves both the oil and natural gas explorers and drillers, and also both on and off-shore drillers – they are kind of energy agnostic. At $67, it is selling for 11.4x 2012 earnings and 10x 2013 earnings.

- Singapore Telecom: Bought in Oct 2012 at US$2.58 or SG$3.15. Up 4.6% since or up 6.8% if we include the dividend that just went ex-div in December 2012. We think SG$3.15 is attractive relative to other Singapore stocks. The price was also temporarily driven down when Temasek sold part of their holdings. The selling is now over and price has recovered a little. But we are not a long term holder in Singtel. It is just a relatively safer alternative in a market that is otherwise expensive.

- OCBC: Acquired in August 2011 at a cost of US$7.56 or SG$9.11. Singapore banks staged a remarkable recovery in 2012. We sold half of it in June 2012. Our holdings is up 24% for the year, but is down 1.3% from our cost.

- M1: Bought early this year at US$1.95 or SG$2.43. Up 14.5% for 2012. We sold half of it in Dec 2012.

- Thai Beverage: We purchased the shares in November 2012 for US$0.33 or SG$0.40. We don't usually invest in stocks which have surged a lot in a year or is near to the all-time high. However, for Thai Bev, we have always like the stock since it was listed but we have never own it until now. In fact, we nearly bought last year when it was selling for SG$0.24 but we were cheap and queued to buy at SG$0.235. For half a cent difference, we miss a huge gain. The other comparable mistake of such is how we miss buying Mastercard and Visa during Dec 2010 and during part of 2011 when we were sucking our thumbs. For Thai Bev, even though the stock is close to its all-time high, we think the valuation is not demanding. It is selling for 16x earnings. What we like is their spirit business which is growing at a good clip, although other parts of the business is holding them back. Compared to other spirit businesses like Brown-Forman and Beam, they are selling well in excess of 20x earnings.

- Marvell Technology: Our biggest loser for 2012 in terms of percentage, and ranks among our all-time biggest losers. We bought at $10.05 and is down by -27.8%. If there is any consolation, it is one of our smallest equity positions. However, we will be holding on given that the price has likely priced in a lot of the bad news which we failed to factor into our analysis. What we thought initially as cheap is perhaps cheap for a reason and probably a value-trap at the time of our purchase. MRVL has about $3.5 a share in cash, so we thought at $10, is selling for 7-8x earnings ex-cash, and if demand for MRVL products recover, it is selling for 5x earnings ex-cash.But what really went wrong for us is not so much on being wrong on the earnings but because we were surprised at how much MRVL is fined when it lost its suit on patent infringement and was fined $1.17 billion for actual damages. Because the infringement is deemed willful, the fine could increase by 3x. In any case, MRVL is appealing, and could overturn the order eventually or lessen the fine tremendously. However, if it doesn't, MRVL hands will be weakened. But we think the fine is outrageous in relation to MRVL revenue and profit. It is one-third of MRVL revenue or 100% of revenue if the punitive damages is levied at 3x of actual damages awarded. We think there's a good chance the actual damages will be eventually reduced.

Google

We foolishly sold

our Google stock as it went up. We fail to get the entire rise. We

bought well but we need to improve our selling. But we did decently

for the short holding period. This is the second time we held and

sold Google. We hardly invest in technology companies

primarily because of their often high stock valuations due to rapid

growth, and potential for obsolescence due to rapid change in

technology. The last thing we want is to pay a high price for a

rapidly growing business that gets swept aside by new technology

shortly after we buy it. Bearing this in mind, it doesn't mean we

wouldn't buy it at all costs. We will buy at the right price,

especially at a bargain price. Any time if Google gets back to $600 -

$650 range, we will be there to buy. At $650, we will be paying about

14x earnings, less if we exclude the cash. Even at $700, it isn't

expensive at 15x eps or less than 13x ex cash. It is hard to find

companies with market leading positions secured by strong competitive

advantages in secular growth markets because such companies do not

usually sell at market multiples. And Google is one such find today.

And this is a business that has top line growth of 20% per year. We

will discuss more if we ever get another chance to purchase Google.

Sometimes we make silly mistakes selling our holdings where we will

be much better, in fact, a lot much better, if we had not sold.

Google is another stock we made a mistake selling in addition to our

recent other mistakes – Davita, Anheuser-Busch Inbev and Amgen. All

of which we bought well but sold atrociously.

Opportunistic

situations

We only managed to

find take advantage of one opportunistic situation when Monster

Beverage took a big heat to its shares in October 2012 when there

were some complaints to FDA that Monster drinks led to some death on

over caffeine consumption. We think it was a “tempest in a teapot,”

to borrow Jamie Dimon's infamous quote. So we purchase some shares at

$42.8 and sold within the same month when the price recovers some of

its losses and lock in gain of 10%. Stock has since surged to almost

back to the pre-plunge price of $51 to $55. Again, we were early in

selling.

Stocks we are considering

Baidu

We

do not usually talk about companies we like that we do not have a

position. Baidu is selling for about $100,

down by a third from the peak more than half a year ago. Now, it has

come to a price we are comfortable in for a growing business. Baidu

business is likely still to be in the early innings. Earnings is

expected to grow in excess of 20%. Valuation is less than 17x for the

next 12 months earnings. If we exclude cash, p/e comes to 15x. For a

business that can grow at mid to high teens level for the medium

term, we think paying 15 to 17x earnings is a good deal. One of the

concern was its market share is eaten up by competitors like Qihoo.

Baidu's market share is down to about 60% from its peak of over 70%.

Baidu's market share used to be in the high 50s to low 60s prior to

Google's exit a couple years ago. Upon Google's exit, Baidu market

share went to over 70%. Now it is back to where it is.

American Movil

Stock is having a rough time and is selling close to 52-week low below $23, priced at 13x earnings. Its domination in Latin America is under pressure from government encouraging more competition, including its homes market, Mexico. We think the price is pretty attractive.

American Movil

Stock is having a rough time and is selling close to 52-week low below $23, priced at 13x earnings. Its domination in Latin America is under pressure from government encouraging more competition, including its homes market, Mexico. We think the price is pretty attractive.

Valeant Pharmaceutical

We think the business is well managed led by one of the smartest mind in the pharmaceutical industry. Valeant pursues a different path from most other large pharmaceuticals. VRX does not spend a large percentage of its revenue on research and development (low single digit versus low to mid teens for major drugs discovery firms) but instead grows through savvy acquisitions that accretes to earnings, sometimes, significantly. They have had much success in the acquisition arena. Even at $60, its all-time high, it is priced at 14.5x 2012 adjusted earnings. It is a rare pharmaceutical that is growing top line and bottom line at such a fast clip at over 20% and 30%, respectively. Although most of the most of the revenue growth came through acquisitions, organic growth is still an industry-leading one at high single to low teens level. Effectively, VRX is a master value investor within the pharmaceutical space. The reason VRX is able to do that it is led by the able Michael Pearson, who has been an extraordinary and aggressive CEO. VRX is a rare find in any industry, which is both a value investor and a savvy operator. The other comparable we can think of are Berkshire Hathaway, any of the Liberty-related companies and Barry Dillar-related companies.

We think the business is well managed led by one of the smartest mind in the pharmaceutical industry. Valeant pursues a different path from most other large pharmaceuticals. VRX does not spend a large percentage of its revenue on research and development (low single digit versus low to mid teens for major drugs discovery firms) but instead grows through savvy acquisitions that accretes to earnings, sometimes, significantly. They have had much success in the acquisition arena. Even at $60, its all-time high, it is priced at 14.5x 2012 adjusted earnings. It is a rare pharmaceutical that is growing top line and bottom line at such a fast clip at over 20% and 30%, respectively. Although most of the most of the revenue growth came through acquisitions, organic growth is still an industry-leading one at high single to low teens level. Effectively, VRX is a master value investor within the pharmaceutical space. The reason VRX is able to do that it is led by the able Michael Pearson, who has been an extraordinary and aggressive CEO. VRX is a rare find in any industry, which is both a value investor and a savvy operator. The other comparable we can think of are Berkshire Hathaway, any of the Liberty-related companies and Barry Dillar-related companies.

VRX is able to generate the types of returns it drives through acquisition largely because of the cost cutting it can achieve in the range of 15% to 20%. As an example, when Valeant merged with Biovail, Biovail was doing a billion dollar sales and in 2012, VRX is targeting to eliminate $300 to $350 million (35% sales) through synergy. So a lot of the $300+ million flows to the bottom line because of the company's low tax structure. In 2011, VRX acquires a number of bolt-on acquisition which in aggregate adds another billion of sales and targets for 25% synergy. Again, a lot of the $250 million is going to flow to the bottom line. So in effect, VRX is generating really high returns by acquiring other businesses in the pharmaceutical industry. VRX has also announced its plan to acquire Medicis which will close in 2013 in a friendly, all-cash deal. The deal will make VRX the largest player in dermatology in the U.S. We like it at $45, and we like it at $50, and now even at $60, we like it, although we have never own it. We intend to and at $60, it is priced at 11x cash earnings.

Of all the 3 stocks listed here where we are interested in, we are most comfortable with Valeant the most.

Subscribe to:

Posts (Atom)